Unsere Organisation hat dank Zuora Revenue bereits einen beträchtlichen Nutzen in Form von Zeitersparnissen und Kostenreduktion erfahren. Sowohl die automatischen Anpassungen der Verträge als auch die umfassenden Aktualisierungen der Daten durch seine benutzerfreundliche Oberfläche haben unsere Arbeitsprozesse grundlegend verändert.

– Anna Lee

Directeur des Revenus, Gainsight

Hat die Dauer der Buchhaltungsabschlüsse um mehr als 30% verringert.

Hat seine durchschnittliche Prüfungszeit um 50% reduziert

Durch Zuora Revenue erlangten wir die essentiellen Echtzeit-Einblicke, die notwendig sind, um manuelle finanzielle Beschränkungen zu eliminieren, unsere Berichterstattung mit entscheidender Präzision zu versehen und schlussendlich wohlüberlegte strategische Entscheidungen zu fällen.

– Chris Gomez

Senior Manager, Revenue Operations, Poly

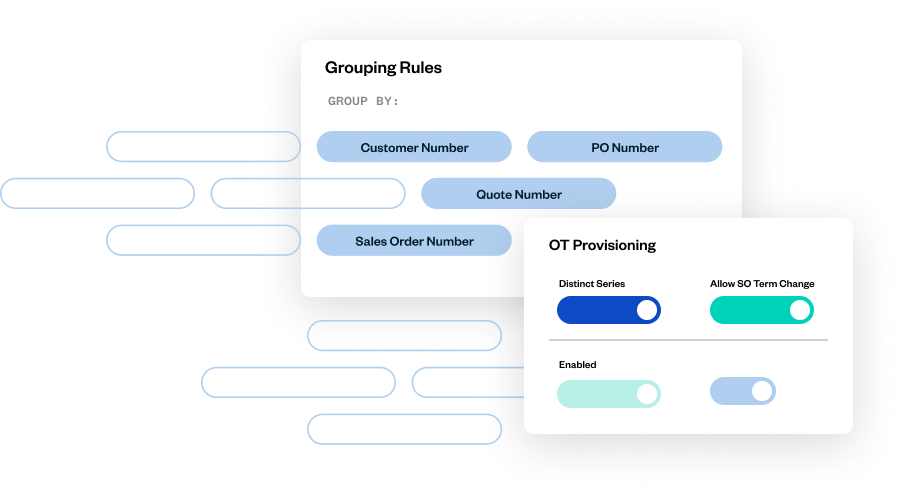

Zuora Revenue wurde gezielt entwickelt, um den spezifischen Anforderungen von Umsatzbuchhaltern gerecht zu werden. Bereits in einem Quartal konnte unser Team signifikante Vorteile verzeichnen. Die Paketkonfiguration verbesserte präzise unsere Umsatzallokationen, das Anpassen von Gruppierungsregeln hat zeitraubende manuelle Abschlusstätigkeiten überflüssig gemacht und die intuitive Benutzeroberfläche steigerte unsere Effizienz durch erweiterte Funktionalität und Bedienkomfort.

– Tony Zhang

Revenue Manager, Nutanix

Mit Zuora Revenue erzielte Nutanix eine jährliche Zeitersparnis von nahezu 550 Stunden